IDFC GOVERNMENT SECURITIES FUND-INVESTMENT PLAN

(Government Securities Fund PF will be merged into

Government Securities Fund IP w.e.f. May 7, 2018)

An open ended debt scheme investing in government

securities across maturities

|

|

|

|

|

IDFC GOVERNMENT SECURITIES FUND-INVESTMENT PLAN

(Government Securities Fund PF will be merged into

Government Securities Fund IP w.e.f. May 7, 2018)

An open ended debt scheme investing in government

securities across maturities

A dedicated gilt fund with an objective to generate optimal returns with high liquidity by investing in Government Securities.

OUTLOOK

The government has been prudent so far in rationing its stimulus

response, focusing first on sustenance and keeping a growth stimulus for

later. Despite the government’s prudence so far, however, the load on

the fiscal is heavy. A necessary condition for financing this is a

well-functioning bond market. The measures announced in August

should now restore normal functioning and allow the substantial

borrowing requirement to start going through without undoing the

transmission channel.

Having said that, it is also true that more than 50% of an INR 20 lakh

crore plus (center and states combined) borrowing program is still

ahead of us. One shouldn’t expect a very large sustainable rally in bonds

basis just the current set of triggers, although one should reasonably

expect most of the recent aggressive sell-off to get unwound. However

re-instatement of orderly functioning now allows participants to start

deploying risk capital with more confidence to take advantage of what

are quite attractive valuations given the underlying backdrop of an

unprecedented growth drawdown and a collapse in credit growth.

The external account is our one significant macro strength today and

provides adequate cushion to RBI to persist with a dovish policy for the

time-being. For all these reasons, our view remains that the important

current pillars of policy will sustain for the foreseeable future. The spike

in inflation presents an interpretation problem for now and it remains our

base case that it will not shift the narrative away from growth for

monetary policy, despite throwing up higher average CPI prints for the

year. In our opinion, focus has to be on best quality AAA and sovereign /

quasi sovereign. There is no macro logic whatsoever for pursuing high

yield strategies.

ASSET QUALITY

FUND FEATURES: (Data as on 31st August'20)

Category: Gilt

Monthly Avg AUM: Rs1,808.55 Crores

Inception Date: 9th March 2002

Fund Manager:

Mr. Suyash

Choudhary (Since 15th October 2010)

Standard Deviation (Annualized): 4.37%

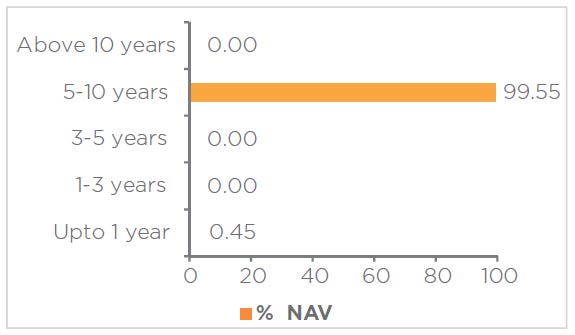

Modified duration: 5.66 years

Average Maturity: 7.39 years

Macaulay Duration: 6.02 years

Yield to Maturity: 6.30%

Benchmark: CRISIL Dynamic

Gilt Index (w.e.f 01st February, 2019)

Minimum Investment Amount: Rs5,000/- and any amount thereafter.

Exit Load: Nil (w.e.f. 15th July 2011)

Options Available: Growth, Dividend - Quarterly, Half Yearly, Annual, Regular & Periodic

Maturity Bucket:

| PORTFOLIO | (31 August 2020) |

| Name | Rating | Total (%) |

| Government Bond | 99.55% | |

| 6.79% - 2027 G-Sec | SOV | 48.42% |

| 7.26% - 2029 G-Sec | SOV | 34.56% |

| 7.17% - 2028 G-Sec | SOV | 16.58% |

| Net Cash and Cash Equivalent | 0.45% | |

| Grand Total | 100.00% |

RISKOMETER

This product is suitable for investors who are seeking*:

• To generate long term optimal returns.

• Investments in Government Securities across maturities

*Investors should consult their financial advisors if in doubt about

whether the product is suitable for them.

|

|

Standard Deviation calculated on the basis of 1 year history of monthly data

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

| Contact your Financial Advisor |

| Call toll free 1800-2-6666-88 |

| Contact your Financial Advisor | Call toll free 1800-2-6666-88 |

Invest online at www.idfcmf.com |  www.facebook.com/idfcamc |

@IDFCMF | |