IDFC DYNAMIC EQUITY FUND

|

|

|

|

|

IDFC DYNAMIC EQUITY FUND

An open ended dynamic asset allocation fund

FUND PHILOSOPHY*

IDFC Dynamic Equity Fund is a hybrid fund with active equity

allocation changing based on the trailing P/E of Nifty 50 index.

The fund has a pre-defined model which indicates the range of

active equity allocation based on P/E levels, and there are 6

different range of equity allocation possible. Higher the P/E band,

lower will be the active equity allocation and vice versa.

Change of bands happen once a month while changes within the

band happen dynamically on a day to day basis. The active equity

portfolio is managed like a diversified fund. Active stock selection

philosophy combines quality stocks with good growth potential.

The quality filters for the fund are – conversion of EBIDTA to

operating cash – OCF as % of EBIDTA > 33%; Moderate leverage:

Debt EBIDTA <3x; Profitability: EBIDTA / Net operating Assets

>30%. Thus, companies which qualify these parameters and have

higher visibility of growth versus peers will form the core

portfolio. Depending on P/E levels, the fund can have more large

or mid/small cap names. The fund will also use Nifty futures to

dynamically manage active equity allocation within a month.

The debt portion of the fund is actively managed. The portfolio

emphasizes on maintaining high credit quality and currently has

100% in AAA or equivalent instruments. Further the portfolio is

oriented towards short-to-medium duration strategies.

Bloomberg Nifty P/E data as of 31st December 2020 indicates a

value of 33 and equity band for the month of January will

continue to be 30-40%

OUTLOOK

• With the spread of the pandemic and the lockdown during Q1

FY21, earnings for the year FY21 were sharply downgraded.

• However, the swifter than expected economic recovery led to a

more robust Q2 FY21.

• Upgrades exceeded downgrades 3x, a rarity, after years of

earnings disappointment.

• FY21 estimates, quickly rebounded from negative to positive

territory, despite the Q1 debacle.

• The fall during Mar’20 lasted less than 35 trading days, erasing

between 36-43% across the indices – Large, Mid and Small Caps.

Supportive action from Central Banks was quicker.

• As investors searched for stable earnings, rotation from one

sector to another, as exhibited from Apr-Dec’20 phase was

evident.

• Staples after outperforming in Mar-Apr, have underperformed

since then. Pharma and IT services outperformed during

May-Sept; Banks/NBFC, after underperforming from

Mar-Sept,20; outperformed during Oct-Dec’20.

• After the debacle of Mar’20, Small caps outshone the rest of the

market – for the first time since CY17.

• If economic recovery is robust and RBI does not move

aggressively into high real interest zone, Small caps could benefit

the most.

FUND FEATURES: (Data as on 31st December'20)

Category: Dynamic Asset Allocation or Balanced Advantage

Monthly Avg AUM: Rs1,263.91 Crores

Inception Date: 10th October 2014

Fund Manager:

Equity Portion : Mr. Arpit Kapoor and

Mr. Sumit Agrawal (w.e.f. 01/03/17)

Debt Portion : Mr. Arvind Subramanian

(w.e.f. 09/11/2015)

Standard Deviation (Annualized): 13.94%

Modified Duration: 2.15 years*

Average Maturity: 2.66 years*

Macaulay Duration:2.23 years*

Yield to Maturity: 4.18%*

*Of Debt Allocation Only

Benchmark: 50% S&P BSE 200 TRI + 50%

NIFTY AAA Short Duration Bond Index

(w.e.f 11/11/2019)

Asset allocation:

Gross Equity (including Arbitrage): 66.44%

Debt: 33.56%

Net Equity: 37.14%

Market Cap Split:

Large Cap: 74.86%

Mid and Small Cap: 25.14%

Minimum Application Amount: Rs5,000/- and any amount thereafter.

Exit Load: In respect of each purchase of Units:

- For 10% of investment: Nil

- For remaining investment: 1% if

redeemed/ switched out within 1 year

from the date of allotment (w.e.f. July 5,2017)

SIP Frequency Monthly (Investor may

choose any day of the month except 29th,

30th and 31st as the date of instalment.)

Options Available: Growth, Dividend

(Payout, Reinvestment and Sweep (from

Equity Schemes to Debt Schemes only))

| PLAN | DIVIDEND RECORD DATE | ₹/UNIT NAV | NAV |

| REGULAR | 18-Dec-20 | 0.12 | 12.1700 |

| 15-Jun-20 | 0.10 | 10.4300 | |

| 28-Jan-20 | 0.15 | 11.3200 | |

| DIRECT | 18-Dec-20 | 0.13 | 13.1400 |

| 15-Jun-20 | 0.11 | 11.1900 | |

| 28-Jan-20 | 0.16 | 12.0800 |

Dividend is not guaranteed and past performance may or may not be sustained in future. Pursuant to payment of dividend, the NAV of the scheme would fall to the extent of payout and statutory levy (as applicable).

| PORTFOLIO | (31 December 2020) |

| Name | Ratings | % of NAV |

| Equity and Equity related Instruments | 66.44% | |

| Net Exposure | 37.14% | |

| Software | 8.02% | |

| Infosys | 6.28% | |

| Infosys - Equity Futures | -1.40% | |

| Tech Mahindra | 2.22% | |

| Tech Mahindra - Equity Futures | -1.19% | |

| Tata Consultancy Services | 2.17% | |

| Tata Consultancy Services - Equity Futures | -2.18% | |

| Wipro | 0.99% | |

| HCL Technologies | 0.71% | |

| Larsen & Toubro Infotech | 0.41% | |

| Banks | 6.80% | |

| ICICI Bank | 4.56% | |

| ICICI Bank - Equity Futures | -1.15% | |

| HDFC Bank | 3.39% | |

| Axis Bank | 1.38% | |

| Axis Bank - Equity Futures | -1.39% | |

| Finance | 5.56% | |

| Muthoot Finance | 1.96% | |

| Muthoot Finance - Equity Futures | -0.17% | |

| Bajaj Finserv | 1.14% | |

| Bajaj Finserv - Equity Futures | -0.51% | |

| HDFC Life Insurance Company | 0.82% | |

| Cholamandalam Invt and Fin Co | 0.73% | |

| Bajaj Finance | 0.60% | |

| Mas Financial Services | 0.43% | |

| Aavas Financiers | 0.38% | |

| ICICI Securities | 0.10% | |

| ICICI Lombard General Insurance Company | 0.06% | |

| Consumer Non Durables | 5.14% | |

| Hindustan Unilever | 1.92% | |

| Hindustan Unilever - Equity Futures | -0.06% | |

| Nestle India | 1.73% | |

| Burger King India | 1.55% | |

| Dabur India | 0.65% | |

| Dabur India - Equity Futures | -0.66% | |

| Tata Consumer Products | 0.40% | |

| Tata Consumer Products - Equity Futures | -0.40% | |

| Pharmaceuticals | 4.62% | |

| Divi's Laboratories | 2.27% | |

| Divi's Laboratories - Equity Futures | -0.39% | |

| Aurobindo Pharma | 2.02% | |

| Aurobindo Pharma - Equity Futures | -0.86% | |

| Cipla | 1.91% | |

| Cipla - Equity Futures | -1.91% | |

| Alkem Laboratories | 1.02% | |

| Dr. Reddy's Laboratories | 0.59% | |

| Dr. Reddy's Laboratories - Equity Futures | -0.59% | |

| IPCA Laboratories | 0.58% | |

| Auto Ancillaries | 3.26% | |

| MRF | 0.94% | |

| MRF - Equity Futures | -0.37% | |

| Minda Industries | 0.93% | |

| Balkrishna Industries | 0.62% | |

| Balkrishna Industries - Equity Futures | -0.55% | |

| Sandhar Technologies | 0.58% |

| Name | Ratings | % of NAV |

| Endurance Technologies | 0.56% | |

| Tube Investments of India | 0.54% | |

| Petroleum Products | 3.21% | |

| Reliance Industries | 5.30% | |

| Reliance Industries - Equity Futures | -2.09% | |

| Telecom - Services | 2.69% | |

| Bharti Airtel | 3.26% | |

| Bharti Airtel - Equity Futures | -0.56% | |

| Cement | 2.28% | |

| UltraTech Cement | 1.20% | |

| JK Cement | 1.09% | |

| Ambuja Cements | 0.47% | |

| Ambuja Cements - Equity Futures | -0.47% | |

| Industrial Products | 1.83% | |

| SRF | 0.84% | |

| Shaily Engineering Plastics | 0.62% | |

| Supreme Industries | 0.62% | |

| AIA Engineering | 0.54% | |

| SRF - Equity Futures | -0.78% | |

| Pesticides | 0.66% | |

| PI Industries | 0.66% | |

| Healthcare Services | 0.59% | |

| Gland Pharma | 0.59% | |

| Gas | 0.47% | |

| Indraprastha Gas | 0.68% | |

| Indraprastha Gas - Equity Futures | -0.21% | |

| Chemicals | 0.43% | |

| Chemcon Speciality Chemicals | 0.43% | |

| Retailing | 0.42% | |

| Avenue Supermarts | 0.42% | |

| Construction | 0.35% | |

| PNC Infratech | 0.35% | |

| Construction Project | 0.32% | |

| Larsen & Toubro | 1.88% | |

| Larsen & Toubro - Equity Futures | -1.89% | |

| KEC International | 0.33% | |

| Index | -9.52% | |

| Nifty 50 Index - Equity Futures | -9.52% | |

| Treasury Bill | 9.00% | |

| 364 Days Tbill - 2021 | SOV | 5.62% |

| 182 Days Tbill - 2021 | SOV | 3.38% |

| Corporate Bond | 7.80% | |

| Reliance Industries | AAA | 3.06% |

| Power Finance Corporation | AAA | 1.97% |

| NABARD | AAA | 1.58% |

| REC | AAA | 1.18% |

| NTPC | AAA | 0.02% |

| Government Bond | 7.56% | |

| 5.22% - 2025 G-Sec | SOV | 3.80% |

| 7.17% - 2028 G-Sec | SOV | 3.76% |

| Commercial Paper | 3.63% | |

| LIC Housing Finance | A1+ | 1.82% |

| HDFC | A1+ | 1.82% |

| Net Cash and Cash Equivalent | 5.57% | |

| Grand Total | 100.00% |

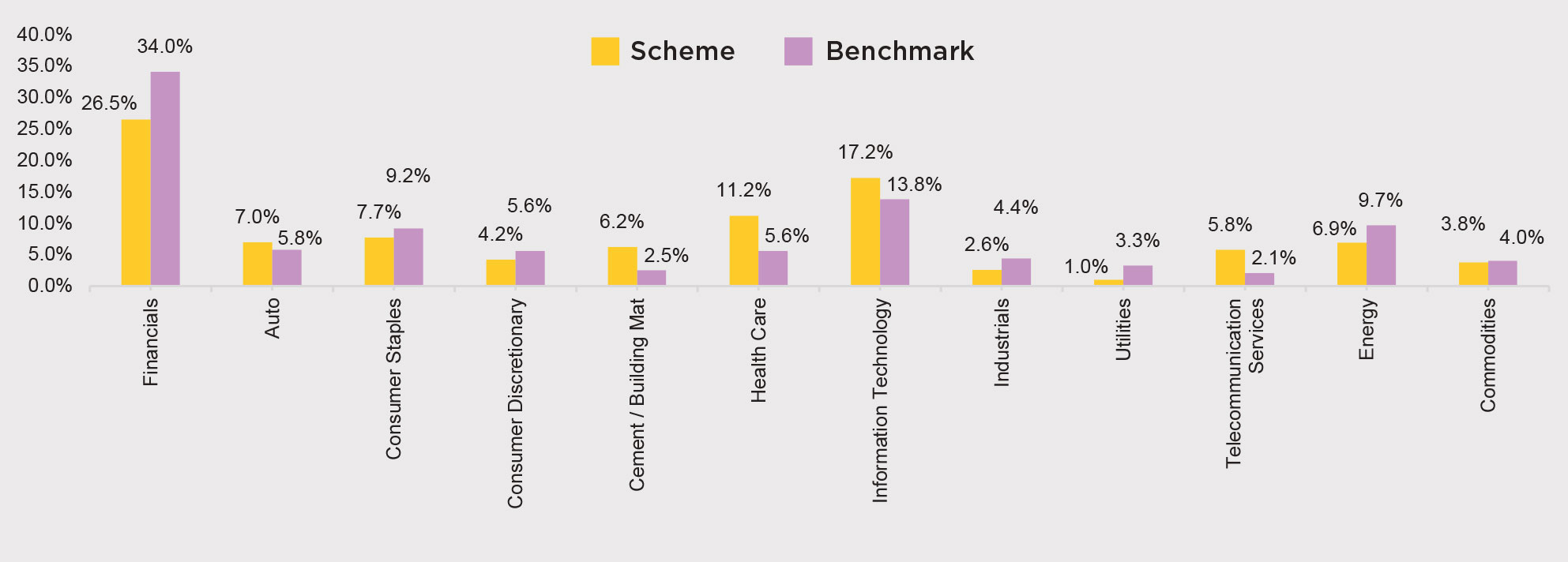

SECTOR ALLOCATION

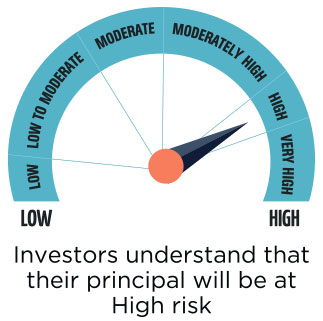

RISKOMETER

This product is suitable for investors who are seeking*:

• To create wealth over long term

• Dynamic allocation towards equity, derivatives, debt and money market instruments

*Investors should consult their financial advisors if in doubt about

whether the product is suitable for them.

|

|

The above mentioned is the current strategy of the Fund Manager. However, asset allocation and investment strategy shall be within broad parameters of Scheme Information Document.

| Contact your Financial Advisor |

| Call toll free 1800-2-6666-88 |

| Contact your Financial Advisor | Call toll free 1800-2-6666-88 |

Invest online at www.idfcmf.com |  www.facebook.com/idfcamc |

@IDFCMF | |