IDFC STERLING VALUE FUND

|

|

|

|

|

IDFC STERLING VALUE FUND

(Previously known as IDFC Sterling Equity Fund w.e.f. May 28, 2018)

An open ended equity scheme following a value investment strategy

IDFC Sterling Value Fund is a value

oriented fund with the current focus on

the mid and small cap segment*.

FUND PHILOSOPHY*

The focus of IDFC Sterling Value Fund has been on building a portfolio of Leader/Challengers and Emerging businesses with an emphasis on bottom up stock selection. As part of the current strategy, the portfolio looks to build on the leaders/challengers – these are the market leaders in the Non-Nifty sectors (like Tyres, Bearings) or Top Challengers in the Nifty sectors (such as FMCG, Banks). The key parameters that we look at while selecting the companies here are low debt to operating cash flow and ROIC (Return on Invested Capital) greater than the Cost of Capital (CoC). The other part of the portfolio focuses on the Emerging Businesses. These are businesses in down cycles or where scale is yet to be achieved or where companies can fund growth without repeated dilutions. Many a times, earnings do not capture fair value of the businesses in down cycles or that are yet to achieve scale and hence popular ratios such as P/E ratio might not be the relevant metric to value the company. Thus, we believe that a better parameter for relative value evaluation could be the Enterprise Value (EV)/Sales ratio & Price/Book (P/B). We also filter stocks for Sustained improvement in RoE (Return on Equity) and RoCE (Return on Capital Employed) and those with Earnings Growth higher than Nifty. This segregation helps in easy management of risk & liquidity aspects of the portfolio.

OUTLOOK

• With the spread of the pandemic and the lockdown during Q1 FY21,

earnings for the year FY21 were sharply downgraded.

• However, the swifter than expected economic recovery led to a

more robust Q2 FY21.

• Upgrades exceeded downgrades 3x, a rarity, after years of earnings

disappointment.

• FY21 estimates, quickly rebounded from negative to positive

territory, despite the Q1 debacle.

• The fall during Mar’20 lasted less than 35 trading days, erasing

between 36-43% across the indices – Large, Mid and Small Caps.

Supportive action from Central Banks was quicker.

• As investors searched for stable earnings, rotation from one sector

to another, as exhibited from Apr-Dec’20 phase was evident.

• Staples after outperforming in Mar-Apr, have underperformed since

then. Pharma and IT services outperformed during May-Sept;

Banks/NBFC, after underperforming from Mar-Sept,20;

outperformed during Oct-Dec’20.

• After the debacle of Mar’20, Small caps outshone the rest of the

market – for the first time since CY17.

• If economic recovery is robust and RBI does not move aggressively

into high real interest zone, Small caps could benefit the most.

FUND FEATURES: (Data as on 31st December'20)

Category: Value

Monthly Avg AUM: Rs2,950.49 Crores

Inception Date: 7th March 2008

Fund Manager:

Mr. Anoop Bhaskar (w.e.f. 30/04/2016) & Mr. Daylynn Pinto (w.e.f. 20/10/2016)

Other Parameters:

Beta: 1.04

R Square: 0.96

Standard Deviation (Annualized): 29.73%

Benchmark: S&P BSE 400 MidSmallCap

TRI (w.e.f 11/11/2019)

Minimum Investment Amount: Rs5,000/- and any amount thereafter.

Exit Load:

• If redeemed/switched out within 365

days from the date of allotment:

➧ Upto 10% of investment:Nil,

➧ For remaining investment: 1% of

applicable NAV.

•If redeemed / switched out after 365

days from date of allotment: Nil. (w.e.f.

May 08, 2020)

SIP Frequency Monthly (Investor

may choose any day of the month

except 29th, 30th and 31st as the date

of instalment.)

Options Available: Growth, Dividend

(Payout, Reinvestment and Sweep

(from Equity Schemes to Debt

Schemes only))

| PLAN | DIVIDEND RECORD DATE | ₹/UNIT | NAV |

| REGULAR | 20-Mar-20 | 0.73 | 12.8800 |

| 16-Feb-18 | 1.38 | 23.2025 | |

| 10-Mar-17 | 1.31 | 18.6235 | |

| DIRECT | 10-Mar-17 | 1.37 | 19.3894 |

| 21-Mar-16 | 1.50 | 16.3433 | |

| 16-Mar-15 | 2.00 | 20.8582 |

Dividend is not guaranteed and past performance may or may not be sustained in future. Pursuant to payment of dividend, the NAV of the scheme would fall to the extent of payout and statutory levy (as applicable).

| PORTFOLIO | (31 December 2020) |

| Name of the Instrument | % of NAV |

| Equity and Equity related Instruments | 98.15% |

| Auto Ancillaries | 8.83% |

| Minda Industries | 2.16% |

| MRF | 2.05% |

| Bosch | 1.91% |

| Tube Investments of India | 1.26% |

| Wheels India | 1.09% |

| Sterling Tools | 0.35% |

| Cement | 8.53% |

| JK Cement | 2.66% |

| The Ramco Cements | 2.00% |

| ACC | 1.64% |

| Prism Johnson | 1.64% |

| Sagar Cements | 0.59% |

| Consumer Durables | 8.05% |

| Voltas | 2.52% |

| Crompton Greaves Consumer Electricals | 1.93% |

| Greenpanel Industries | 1.32% |

| Greenply Industries | 1.18% |

| Butterfly Gandhimathi Appliances | 1.10% |

| Software | 7.04% |

| Birlasoft | 2.84% |

| Persistent Systems | 1.88% |

| KPIT Technologies | 1.20% |

| HCL Technologies | 1.12% |

| Finance | 6.86% |

| Mas Financial Services | 2.17% |

| ICICI Lombard General Insurance Company | 2.16% |

| ICICI Securities | 1.96% |

| Magma Fincorp | 0.57% |

| Pharmaceuticals | 6.70% |

| IPCA Laboratories | 2.67% |

| Aurobindo Pharma | 2.34% |

| Alembic Pharmaceuticals | 1.05% |

| Dishman Carbogen Amcis | 0.64% |

| Consumer Non Durables | 6.20% |

| Emami | 2.44% |

| Tata Consumer Products | 1.90% |

| Radico Khaitan | 1.86% |

| Banks | 5.59% |

| ICICI Bank | 3.99% |

| RBL Bank | 1.60% |

| Construction Project | 5.37% |

| KEC International | 3.20% |

| NCC | 2.17% |

| Industrial Products | 5.19% |

| Bharat Forge | 1.73% |

| Polycab India | 1.40% |

| Graphite India | 1.39% |

| SRF | 0.67% |

| Ferrous Metals | 4.80% |

| Jindal Steel & Power | 2.89% |

| Maharashtra Seamless | 1.01% |

| Kirloskar Ferrous Industries | 0.90% |

| Chemicals | 3.83% |

| Deepak Nitrite | 3.83% |

| Industrial Capital Goods | 3.00% |

| Bharat Electronics | 1.62% |

| CG Power and Industrial Solutions | 0.97% |

| Skipper | 0.40% |

| Hotels/ Resorts and Other Recreational Activities | 2.58% |

| The Indian Hotels Company | 1.91% |

| EIH | 0.67% |

| Gas | 2.55% |

| Gujarat Gas | 2.55% |

| Retailing | 2.47% |

| V-Mart Retail | 1.55% |

| Aditya Birla Fashion and Retail | 0.92% |

| Textiles - Cotton | 2.40% |

| Vardhman Textiles | 1.78% |

| Nitin Spinners | 0.62% |

| Textile Products | 1.96% |

| K.P.R. Mill | 1.40% |

| Dollar Industries | 0.57% |

| Power | 1.78% |

| Kalpataru Power Transmission | 1.18% |

| Nava Bharat Ventures | 0.59% |

| Transportation | 1.65% |

| VRL Logistics | 1.65% |

| Petroleum Products | 1.48% |

| Bharat Petroleum Corporation | 1.48% |

| Pesticides | 1.13% |

| Rallis India | 0.76% |

| PI Industries | 0.37% |

| Media & Entertainment | 0.16% |

| Entertainment Network (India) | 0.16% |

| Net Cash and Cash Equivalent | 1.85% |

| Grand Total | 100.00% |

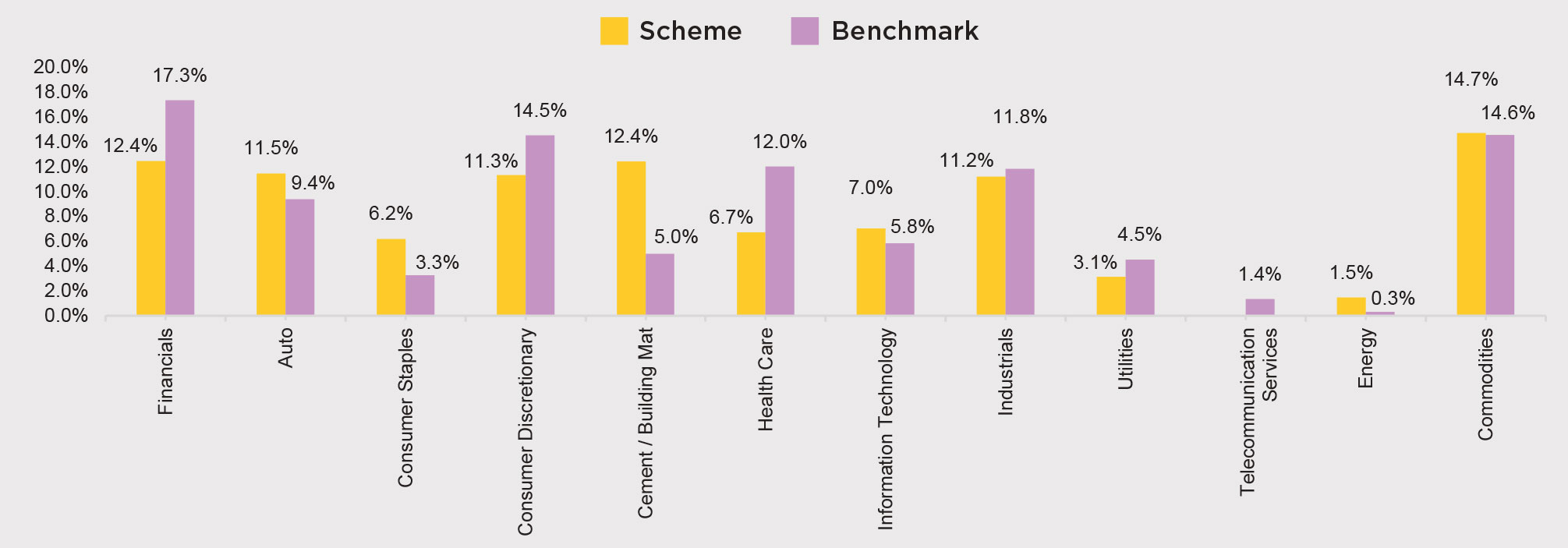

SECTOR ALLOCATION

RISKOMETER

This product is suitable for investors who are seeking*:

• To create wealth over long term

• Investment predominantly in equity and equity related instruments

following a value investment strategy

*Investors should consult their financial advisors if in doubt about

whether the product is suitable for them.

|

|

The above mentioned is the current strategy of the Fund Manager. However, asset allocation and investment strategy shall be within broad parameters of Scheme Information Document.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

| Contact your Financial Advisor |

| Call toll free 1800-2-6666-88 |

| Contact your Financial Advisor | Call toll free 1800-2-6666-88 |

Invest online at www.idfcmf.com |  www.facebook.com/idfcamc |

@IDFCMF | |