IDFC DYNAMIC BOND FUND

|

|

|

|

|

IDFC DYNAMIC BOND FUND

An open ended dynamic debt scheme investing across duration

The fund is positioned in the dynamic bond fund

category to take exposure across the curve

depending upon the fund manager’s underlying

interest rate view where we employ the majority of

the portfolio. It is a wide structure and conceptually

can go anywhere on the curve.

OUTLOOK

• If the factors supporting India’s cyclical rebound come to fruition, a lot of

macro-economic headaches feared at the beginning of the year will ease.

Thus some of the fiscal inflexibilities and associated risks of sovereign

rating downgrades will abate, the external account will build even further

buffers as capital flows remain strong, and hopefully India’s appeal will

percolate to global fixed income investors as well.

• Monetary policy will gradually move from the level of emergency level

accommodation today to one of still high accommodation. This will likely

be a slow process and will involve more discretionary adjustments to the

price of liquidity rather than the quantity of it.

• Yield curves will gradually bear flatten. It is very likely that the bulk of this

adjustment will be made by the very front end rates. This is not to say that

long end rates won’t have to adjust. Rather, the quantum of adjustment

there may be of a relatively smaller magnitude when compared with rates

at the very front end.

• The starting point today is one of a very steep yield curve. Thus unlike in

normal times when the yield curve is quite flat, the decision on duration

isn’t a binary one any more. Rather, one has to examine the steepness of

the curve and position at points where the carry adjusted for duration

seems to be the most optimal.

• Credit spreads, including on lower rated assets, have compressed

meaningfully. These reflect the chase for ‘carry’ in an environment of

abundant liquidity and funds flow, as well as the relatively muted supply of

paper as companies have belt tightened and focused on cash generation.

As activity resumes over the year ahead, issuances will likely increase

thereby pressuring spreads to rise.

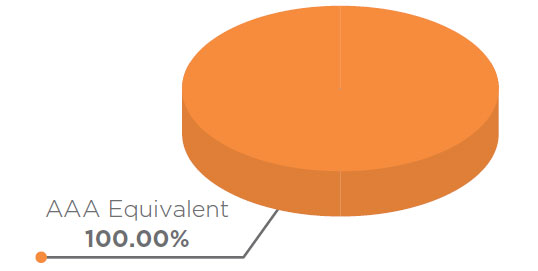

ASSET QUALITY

FUND FEATURES: (Data as on 31st December'20)

Category: Dynamic Bond

Monthly Avg AUM: Rs3,043.49 Crores

Inception Date: 25th June 2002

Fund Manager:

Mr. Suyash

Choudhary (Since 15th October 2010)

Standard Deviation (Annualized): 4.13%

Modified duration: 5.27 years

Average Maturity: 6.85 years

Macaulay Duration: 5.42 years

Yield to Maturity: 5.76%

Benchmark: CRISIL Composite Bond

Fund Index

Minimum Investment Amount: Rs5,000/- and any amount thereafter.

Exit Load: Nil (w.e.f. 17th October

2016)

Options Available: Growth, Dividend -

Periodic, Quarterly, Half Yearly, Annual

and Regular frequency (each with

Reinvestment, Payout and Sweep

facility)

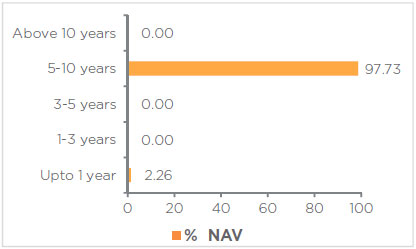

Maturity Bucket:

| PORTFOLIO | (31 December 2020) |

| Name | Rating | Total (%) |

| Government Bond | 97.74% | |

| 7.26% - 2029 G-Sec | SOV | 32.95% |

| 6.79% - 2027 G-Sec | SOV | 31.08% |

| 8.24% - 2027 G-Sec | SOV | 30.92% |

| 7.17% - 2028 G-Sec | SOV | 1.82% |

| 6.97% - 2026 G-Sec | SOV | 0.69% |

| 6.45% - 2029 G-Sec | SOV | 0.27% |

| 8.20% - 2025 G-Sec | SOV | 0.004% |

| Net Cash and Cash Equivalent | 2.26% | |

| Grand Total | 100.00% |

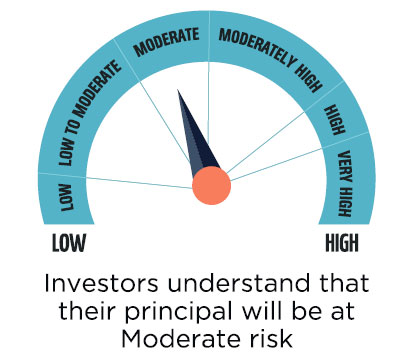

RISKOMETER

This product is suitable for investors who are seeking*:

• To generate long term optimal returns by active management

• Investments in money market & debt instruments including G-Sec across duration

*Investors should consult their financial advisors if in doubt about

whether the product is suitable for them.

|

|

Standard Deviation calculated on the basis of 1 year history of monthly data

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

| Contact your Financial Advisor |

| Call toll free 1800-2-6666-88 |

| Contact your Financial Advisor | Call toll free 1800-2-6666-88 |

Invest online at www.idfcmf.com |  www.facebook.com/idfcamc |

@IDFCMF | |